LMM BLOG

ART AS AN ASSET CLASS

VALENTIN KENNDLER

is an art consultant and court-certified expert for “art after 1945”. He supports his business partners in buying and selling art objects.

www.contemporaryartadvisors.com

Can art be considered an investment?

Art is first and foremost art. But “secondarily”, art – in certain areas – works very well as an investment. Especially in times when many real investments are already quite “hyped”. The art market is still far from that.

What is the minimum investment amount and when does it make sense (as an investment)?

It is always a question of the “risk / return” ratio at which one feels comfortable. In principle, it starts at EUR 5,000 for “emerging art”. Valuable and liquid investments start at EUR 50,000.

How do you deal with issues such as the lack of transparency, valuation models, market / stock exchange as an investor?

That’s a lot of questions at once, about which entire books have been written. The art market is quite a “Wild West” in many areas. But of course – if you know your way around – that can be a great advantage. We support our clients in precisely this point: they usually have their expertise in other areas, and also don’t have an infinite amount of time. With our support, however, they shop like professionals and also have all the access.

Are there any indices for the development of the art market that investors can use as a guide? How have they developed?

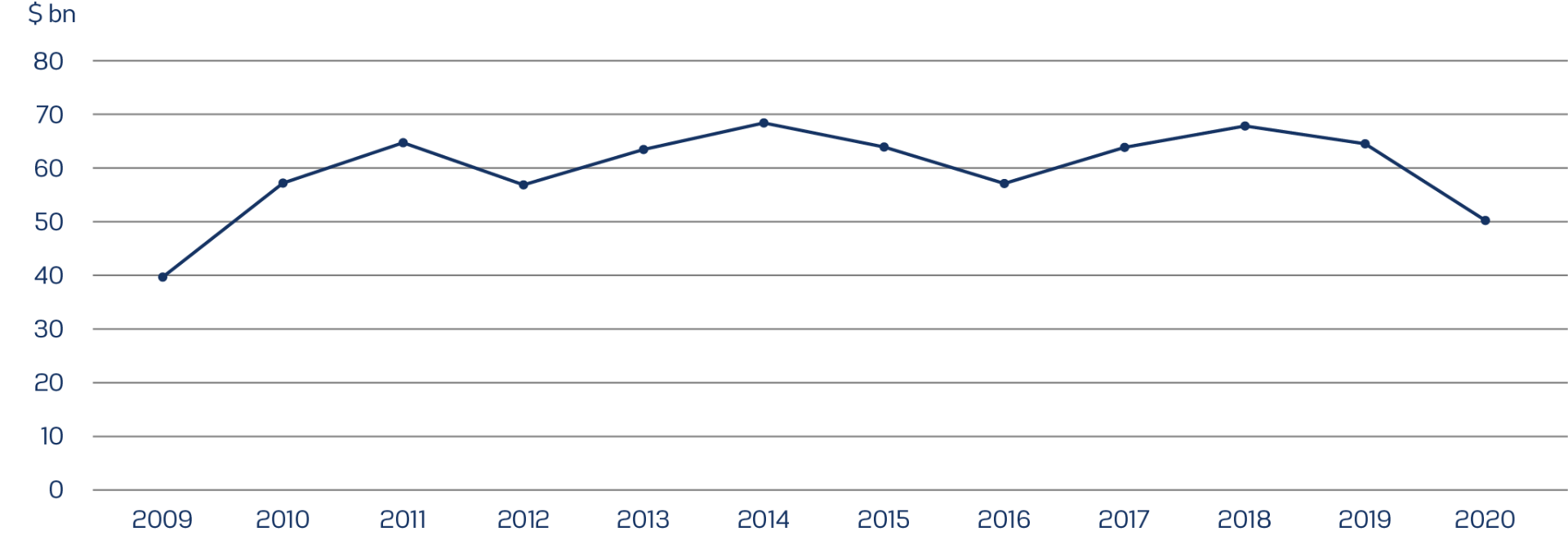

Yes, there are. There are indices from artprice, from Sotheby’s, from UBS and many others. The latter says that prices have risen by 62 % from 2009 – 2019. In 2020 we saw a decent decrease in prices.

Is art currently expensive or in which segments are there opportunities for investors?

Unlike some other “alternative investments”, art has not gone through the roof. And yes, we get offers on the table every day, some of them are real opportunities. Even if you calculate it complete transparently and objectively.

How do I value art?

Usually on the basis of comparative values. But often you have to be very familiar with an artist to know what is comparable.

Do the lack of investment alternatives also lead to an increase in demand for art?

We felt that very clearly in 2020. Definitely. Many people don’t necessarily want to have their money in the bank account, so art sometimes becomes a topic.

How did prices develop in the “Corona year” 2020?

If you look at the entire art and antiques market, the volume fell by around 25% in 2020. Of course, prices are also under pressure, which is in principle good for buyers. But you have to look very carefully: In a crisis, you don’t sell the crown jewels first but tend to sell the “leftovers”. By the way, online sales have doubled.

What are the current trends?

Well, the prices of “Banksy” have really gone through the roof. For a “Girl with Balloon” in an edition of 600, you currently pay over USD 200,000. The state of preservation is very relevant. The field of “digital art” is interesting in the long term. The blockchain and non-fungible tokens (NFTs) offer interesting possibilities for the future. Most recently, a record sum of USD 69.3 million was paid at a Christie’s auction for the work “The First 5000 Days” by the digital artist Beeple. It becomes apparent that there is a lot of attention here.

The global art market 2020 in figures:

- Global art and antiques sales have reached USD 50.1 bn, down 22 % vs. 2019.

- Online sales have reached a record 12.4 bn, a doubling compared to the previous year. The online market share is 25 % for the first time.

- US, UK and China account for 82 % of global sales.

The US market is the largest market with a share of 42 %.

Source: Art Basel & UBS Report 2021

The global art market: Value of transections

LMM COMPASS

With our newsletter we provide information about the current situation on the financial markets, current investment topics and LMM.