LMM BLOG

INFLATION – COME TO STAY?

Inflation rates have retreated recently and the rapid rise in inflation, particularly due to the energy shock in 2022, is losing steam. The development is being watched with argus eyes by central banks and investors, as inflation is still there and well above the central banks' targets.

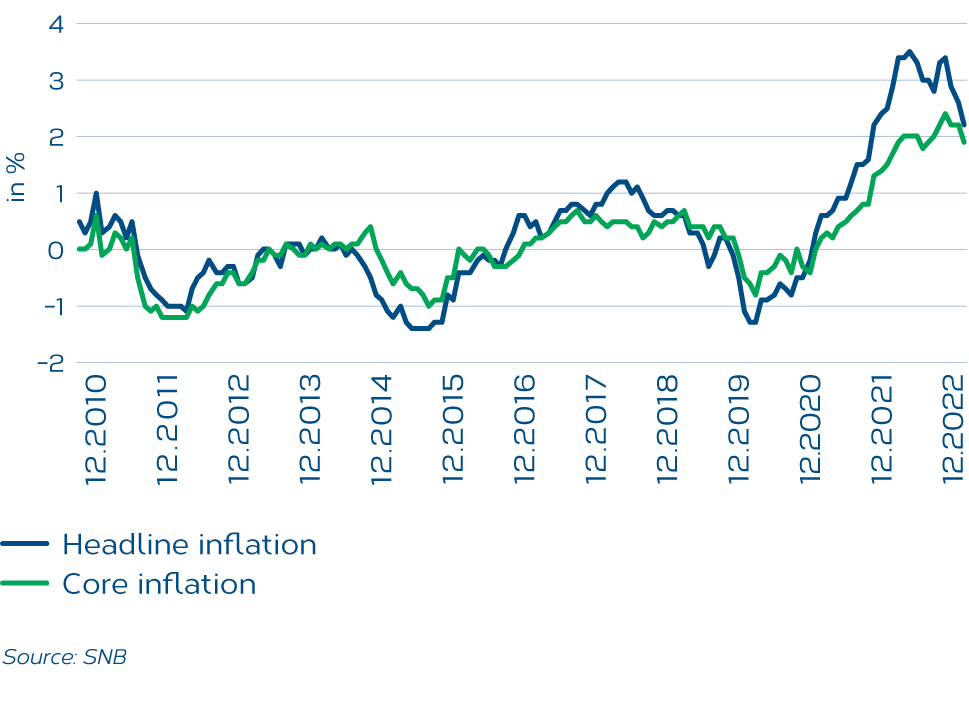

Headline and core inflation CH

The SNB has defined a range of 0 to 2 % as its target value. The ECB and the FED are aiming for a mediumterm target value of 2 % p.a. As per today, the core rates, especially in Europe and the USA, are still well above the target values.

Experts and central bank representatives have pointed out that inflation spreads in spurts across the economy as a whole as players try to pass on costs. In this context, one also speaks of second-round effects, which are currently particularly noticeable in the services sector.

At the most recent central bank meetings, further interest rate hikes (Switzerland and Europe) were decided or planned adjustments were indicated (USA). The central banks expect a stubborn core rate which will only recede slowly. They intend to counter this development with determination and to raise interest rates further if necessary.

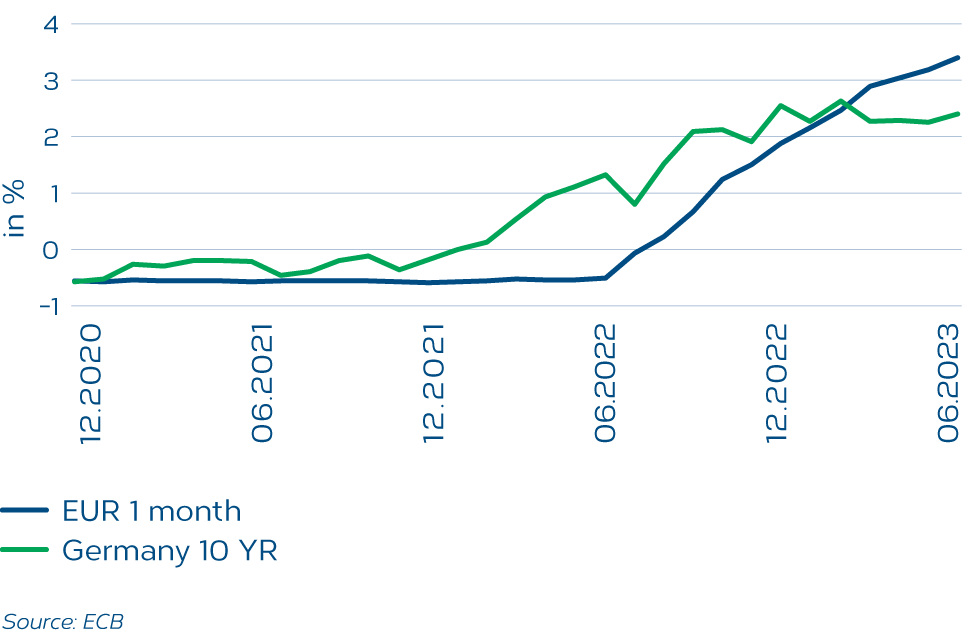

Interest rate developments on key rates and ten-year government bonds in EUR

After several years of low interest rates, an abrupt and rapid rise in interest rates can be seen since 2022. The new interest rate reality is now affecting economic development with a certain delay. On the part of the experts, it is expected that the economy will weaken. This expectation is also reflected in the financial markets. For example, in the case of bonds, short-term rates are higher than longer-term rates.

Conclusion: What points can be noted?

• As far as inflation is concerned, it is not (yet) possible to sound the all-clear. The second-round effects are taking effect and ensure that, according to central bank expectations, the core rate will decline only sluggishly.

• The central banks have communicated as follows with regard to possible further steps:

SNB: "...it cannot be ruled out that additional rate hikes will be necessary..."

ECB: "...raise key interest rates to a sufficiently restrictive level and maintain this level for as long as necessary."

• Central banks have raised interest rates within a very short period of time and in large steps. Imagine, for example, that the ECB has raised rates by a remarkable 400 basis points (or 4 %) since last July.

• The new "interest rate world" will have a negative impact on economic development, but when and to what extent is difficult to assess at the moment. For this reason, the majority of central banks (with the exception of Japan) are sticking to their restrictive policies. A sharp downturn in the economy could prompt the central banks to abandon the path they have taken to date.

LMM COMPASS

With our newsletter we provide information about the current situation on the financial markets, current investment topics and LMM.