LMM BLOG

MSCI AC WORLD INDEX – WHAT SHOULD YOU KEEP IN MIND WHEN INVESTING PASSIVELY

In recent years, an increased trend toward indexproximate implementation in asset investment has been observed, particularly among institutional investors. The global equity index MSCI AC World is often chosen as the benchmark for passive implementation. Below, we analyze the characteristics of this index regarding its composition, inclusion criteria, weighting method, and concentration risks.

What is the composition of the MSCI AC World Index?

This global equity index tracks the performance of companies from 23 developed markets and 24 emerging markets, focusing on established, large-cap companies (the top 70 %) and mid-cap companies (the subsequent 15 %). Small-cap companies are excluded. This covers approximately 85 % of the globally investable equity market. Each company is assigned to one of a total of 11 sectors.

What is the weighting methodology?

The weighting of individual companies follows a clear, automatic logic. Only the amount of shares freely tradeable on the stock exchange (free float) counts. Since there are no quotas for specific countries or industries, the index dynamically reflects the actual current market value ratios. MSCI reviews the index four times a year – in February, May, August, and November. New additions, changed ownership structures, or shifted market capitalizations are updated automatically, without anyone actively or arbitrarily intervening in the rulebook in between.

What is the consequence of this weighting method?

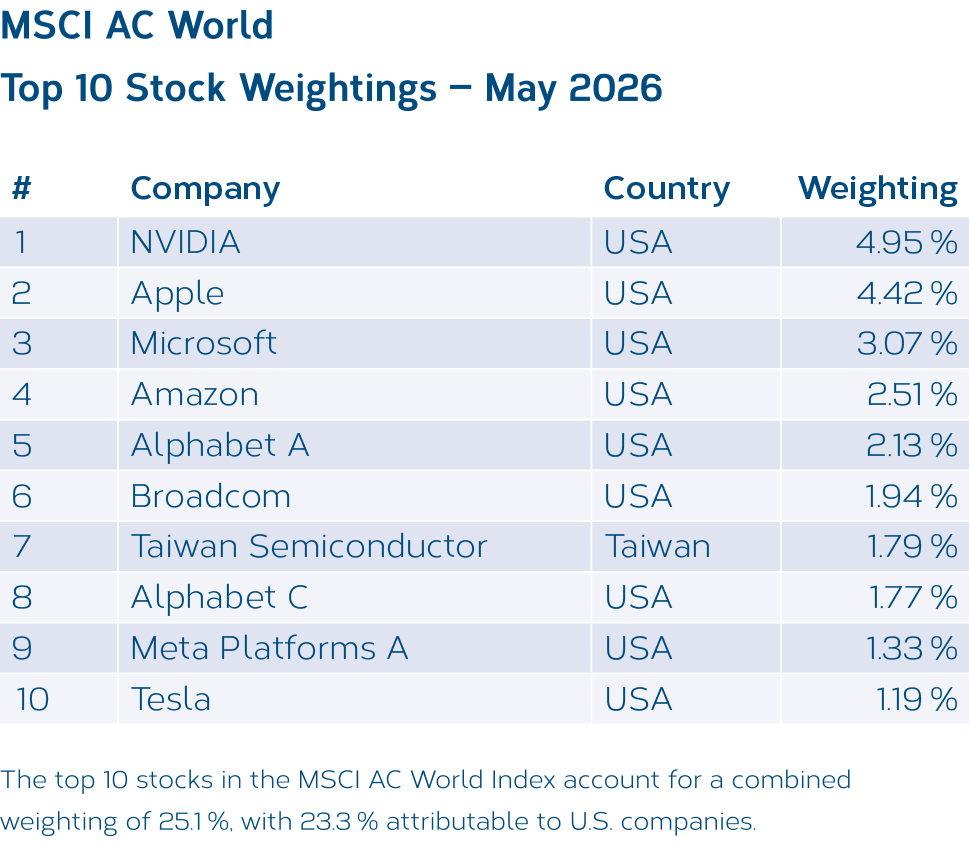

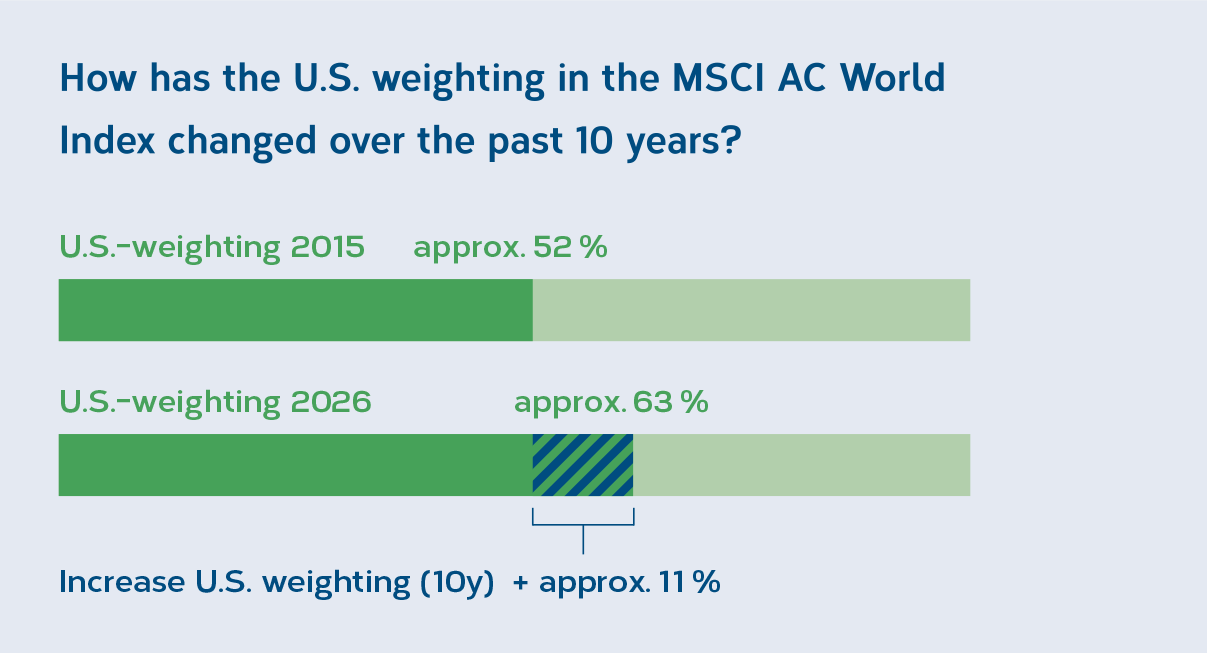

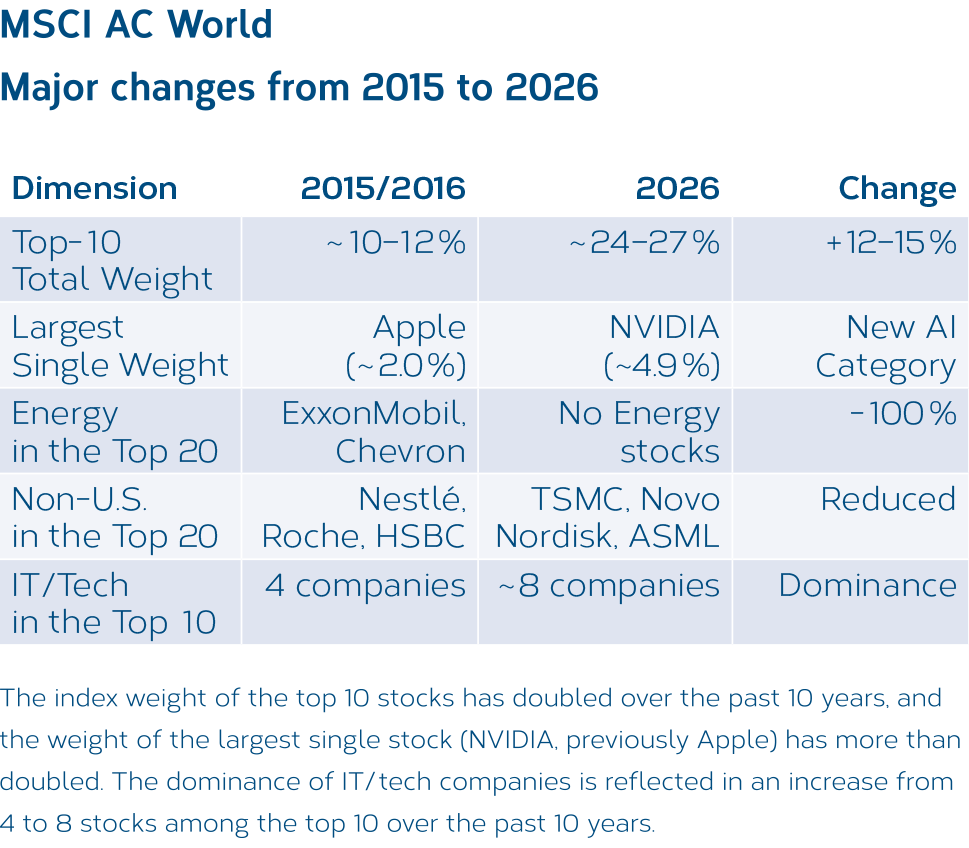

This automatic weighting also has a downside: companies and markets with a high market value and strong price performance – such as the US and the technology sector at present – increasingly dominate the index. The system functions like an amplifier: the better these 'giants' perform, the heavier their weight becomes in the index. As a result, concentration risks inevitably build up.

What were the main drivers of this U.S. dominance?

The main reason for this 'US boom' lies in the differing performance of the individual sectors. The US market is dominated by hyper-growth technology and communication companies. In contrast, Europe and emerging markets are characterized more by classic value sectors, such as banking, energy, or materials. The US tech giants – most notably the well-known 'Magnificent 7' – have achieved significantly more dynamic earnings growth. Sectors like cloud computing, semiconductors, and artificial intelligence (AI) are experiencing an unprecedented boom. Another driver over the last 10 years: US companies repurchased their own shares to a historically unprecedented extent, which further pushed stock prices up massively.

Conclusion

The historically strong return of the global equity index MSCI AC World is largely attributable to the strong performance of the heavily weighted US tech sector. Anyone investing passively in this index today makes themselves highly dependent on the performance of a few US tech companies. For those who wish to reduce this concentration risk while remaining passively invested, several alternatives are outlined below:

- Weighting by Economic Output (GDP Approach)

Here, it is not market value that counts, but actual economic output. As a result, the US share automatically drops to around 30 %. - Equal Weighted

Every company in the index receives exactly the same weight – regardless of its market value. The US share shrinks to approximately 23 % here. - Multi-Factor Approach

This approach filters and weights companies based on specific characteristics, such as value, quality, momentum, and company size (mid-cap and small-cap companies). - The World Without America

The global equity index MSCI AC World ex USA excludes the US entirely. This gives you the freedom to manage the US portion yourself via a separate product and cap it with a fixed upper limit.

LMM COMPASS

With our newsletter we provide information about the current situation on the financial markets, current investment topics and LMM.